Canadians malls, while in better shape than their American counterparts, are nonetheless facing headwinds. Many anchor tenants such as Sears and Target have closed down in recent years, consumers are increasingly ordering what they see in-store on their phones, and decreasing car ownership rates make it harder for malls to attract shoppers. Those are just a few of the trends shopping centre operators have to deal with if they want to stay relevant.

In Canada, 4 square feet per inhabitant is dedicated to shopping centres, compared to 23.5 in the US. In short, malls north of the border are doing better because they have less excess space. Regardless, they still face the same hurdles.

In the long run, however, decreasing the square footage of malls is no invincible moat for the Canadian malls. Shoppers no longer need to physically go to a mall to purchase the items they want, and having anchor tenants and providing ample parking spaces are decreasingly sustainable strategies for staying relevant.

Canadian mall owners took notice. In order to maintain relevance in this ever-changing environment, they are redefining the mall experience. Rather than merely being a place people go to buy things, malls are striving to be a place where people go to enjoy themselves. To do so, they’re adding entertainment and high-end dining to their offerings and investing in technologies that allow them to better serve shoppers. They are moving away from being a general shopping destination and trying to stand out as a destination in their own right.

Despite the headwinds, the story of Canadian shopping malls is one of resilience and ingenuity. As a result, while the mall square footage per inhabitant may drop, Canadian malls are not going away. They’re just going to look a lot different from the teenage hang-outs of the pre-internet era.

Malls lost their biggest appeal when online retailers started simultaneously offering a wide range of products and providing additional shopping convenience. Mall aisles stopped meeting modern shoppers’ expectations for a memorable and exciting shopping experience.

Since then, top Canadian performers reinvented themselves in order to provide a vivid, colourful and sensory experience. Shopping malls are now turning into recreational destinations where consumers not only shop, but also visit to spend time with their friends and family.

For mall managers, the equation is crystal clear: more time spent in the mall translates to additional purchases, better conversion rates, and repeat business.

Consumers expect more — they desire more than mere shopping. They want a unique experience. Those who strive to provide that kind of environment offer an exclusive shopping offering, high-end entertainment and haute cuisine.

Some are likening the new mall experience to a playground or theme park that meets consumers’ sensory needs. A prime example of this is Cirque du Soleil. They recently announced they are launching family entertainment centres in malls across Canada in partnership with real estate company Ivanhoé Cambridge.

To make the best use of all their space, malls are now extending their offerings to include co-working spaces. In Mississauga, the Mindshare Workspace is a 4,000 square-foot flexible workspace for startups and local businesses. A developer approached the Mindspace founder and there are plans to create more workspaces in other malls across Canada.

With the new mall experience, you can literally work, shop and play in one place. When it comes to shopping, Millennials represent a huge target market, making up approximately 26 percent of the Canadian population, or about 9 million people. Their shopping journey is highly technology-based. Online shopping plays a part in this, but their decision-making as consumers is also heavily-based on social media hype or popularity. Malls can leverage this by offering pop-up spaces that provide products trending on social media.

Pop-ups enable malls to generate excitement with consistent new offerings rather than locking companies into leases. With the right offerings, tactics like these can lead to long lines of consumers, eagerly waiting to purchase. Toronto’s Yorkdale centre created CONCEPT, a 3,600 square foot multi-tenant space devoted to pop-ups.

Shopping is one major aspect, however opportunities to keep people in the mall to continue socializing after they have finished shopping also need to be tapped into. Food courts used to offer run-of-the-mill fast food but consumers have grown more health-conscious and palettes have become more diverse and demanding. In response, sit-down dining and upscale options are being introduced.

Extending entertainment options is a surefire way to make the mall a social destination. A prime example of this in Canada is The Rec Room, which opened one of its locations at the West Edmonton Mall. Marketed as “Eats and Entertainment,” it offers exactly that with a wide range of activities, including gaming, gambling and even bowling. Sports enthusiasts can come and watch games on big screens and a program offering live concerts and comedy is also on the menu.

Coupled with Canadian-inspired food from brunch to dinner options, they aim to cater to every taste and age group from family outings to after-work drinks and weekend late nights. There are currently five Rec Room locations in Alberta and Ontario, with plans to open 15 more across Canada. As the mall experience continues to evolve, they are quickly becoming a one-stop playground, providing every consumer need under one roof.

People don’t just shop anymore. They want to live an experience. It isn’t just a buzzword: shopping centres are increasingly shifting towards experiential retail.

There’s an ongoing joke that there are more submarines in the West Edmonton Mall than in the entire Canadian navy. The biggest mall in the country remains the largest tourist attraction in Alberta — even surpassing Banff! Since its construction in 1981, it has grown to hold amusement parks, hotels, and the second largest indoor water park in the world. It even hosts special events such as an indigenous culture festival and a comedy fest, friendly dog races, video game competitions, hockey games, and more.

Experiential retail is a worldwide phenomenon. Ivanhoé Cambridge, a subsidiary of Caisse de dépôt et placement du Québec, will soon launch 2,200 square metre (24,000 square feet) family-friendly entertainment centres in collaboration with Cirque du Soleil.

Westfield, the British shopping centre chain, dedicates entire areas to family spaces and open-air activities. The Mall of the Emirates in Dubai is famous for its indoor ski centre. In the United Sates, the 90 biggest malls spent over $8 billion USD in renovations in four years, enhancing their shopping centres with children’s theatres, cooking centres, bowling alleys, arcades, billiard rooms, indoor rock climbing walls, lounges for Uber clients, and, notably, stages for concerts and shows. Since 2012, 13% of the real estate within American malls has nothing to do with shopping.

Shopping centres that offer entertainment, childcare or high-end dining achieve the highest sales. According to the magazine Campaign, a successful business is more akin to a cinema.

Cirque du Soleil is setting up shop in MallsNext year, Cirque du Soleil Entertainment Group will be adding family entertainment centres to its portfolio of creative projects. They have developed an innovative concept for indoor family entertainment specially designed for retail locations. The recreational centres will offer a brand new immersive family experience, where people can stretch their imaginations and explore newfound circus skills. The indoor centres will be installed in premium immersive spaces covering about 24,000 square feet and will offer a wide range of acrobatic, artistic and other Cirque du Soleil-inspired recreational activities, such as bungee jumping, aerial parkour, wire and trampolines, mask design, juggling, circus track activities, dance and more. It has partnered with Ivanhoé Cambridge to launch its first CREACTIVE indoor centre in the world, set to open in September 2019 in the Greater Toronto Area. |

As malls are turning into entertainment centres, the traditional food court is getting a makeover. Malls now strive to offer their customers a higher-quality food experience, with better restaurants establishing themselves in shopping centres.

“Shopping centre dining is up considerably in the US and you can see major malls are going to lease to larger restaurants that are destinations, said Michael Kehoe, a retail specialist with Fairfield Commercial Real Estate in Calgary. The concept of ‘eatertainment,’ where people can go and have an experiential meal — that’s going to become more and more evident in Canada for sure.”

Darryl Schmidt, vice-president of national leasing for Cadillac Fairview, agrees fine dining is increasingly being offered in Canadian malls: “In the last three years, we’ve increased the amount of premium, casual restaurants in our shopping centres by 35 percent and that’s going to continue. That’s not a fad. That’s a trend. We’re going to continue to increase the amount of dining options, both on a fast food basis with food halls and with premium casual restaurants.”

20%

The total real estate space dedicated to food &

beverage will reach 20% by 2025 in the global market.

Source: International Council of Shopping Centers.

Canadians malls are extending their recreational offering and finding innovative ways to attract and retain shoppers. Yet, the gap between high and low performers is still widening. Successful venues such as Yorkdale in Toronto welcome up to 18 million savvy consumers each year while other malls are being abandoned. So what is happening? In one word: specialization.

The one-size fits all department store strategy is no longer relevant as the middle class explodes into many different consumer cohorts with different needs and purchasing behaviours.

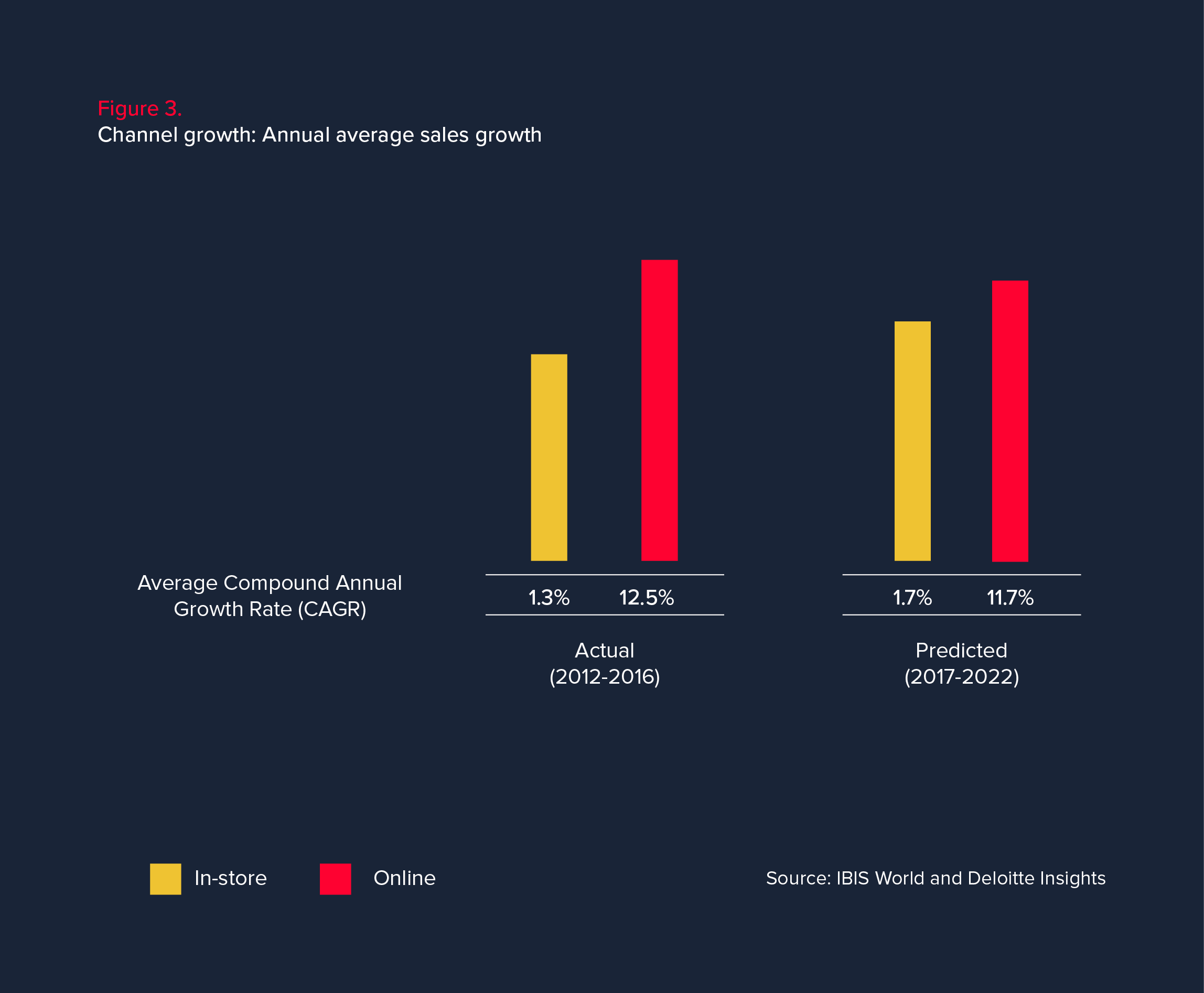

Since 2012, retail sales in North America have been climbing — both online and in-store. In absolute terms, the growth of physical retail (brick and mortar) contributes to half of the market’s entire growth.

That’s one of the interesting facts that emerges from The Great Retail Bifurcation, a Deloitte study that cross-references American macroeconomic data and consumer socio-demographic profiles to decipher the trends that are going beyond this e-commerce vs. brick and mortar battle.

40.8%

In Canada, the 20% richest segment of the population

held more than 40.8% of total incomes.

Source: World Bank

Thus, if all of the economic indicators are increasing, the true riddle of today’s market is this: how did retail get its floundering reputation in a time when its ground is clearly so prolific?

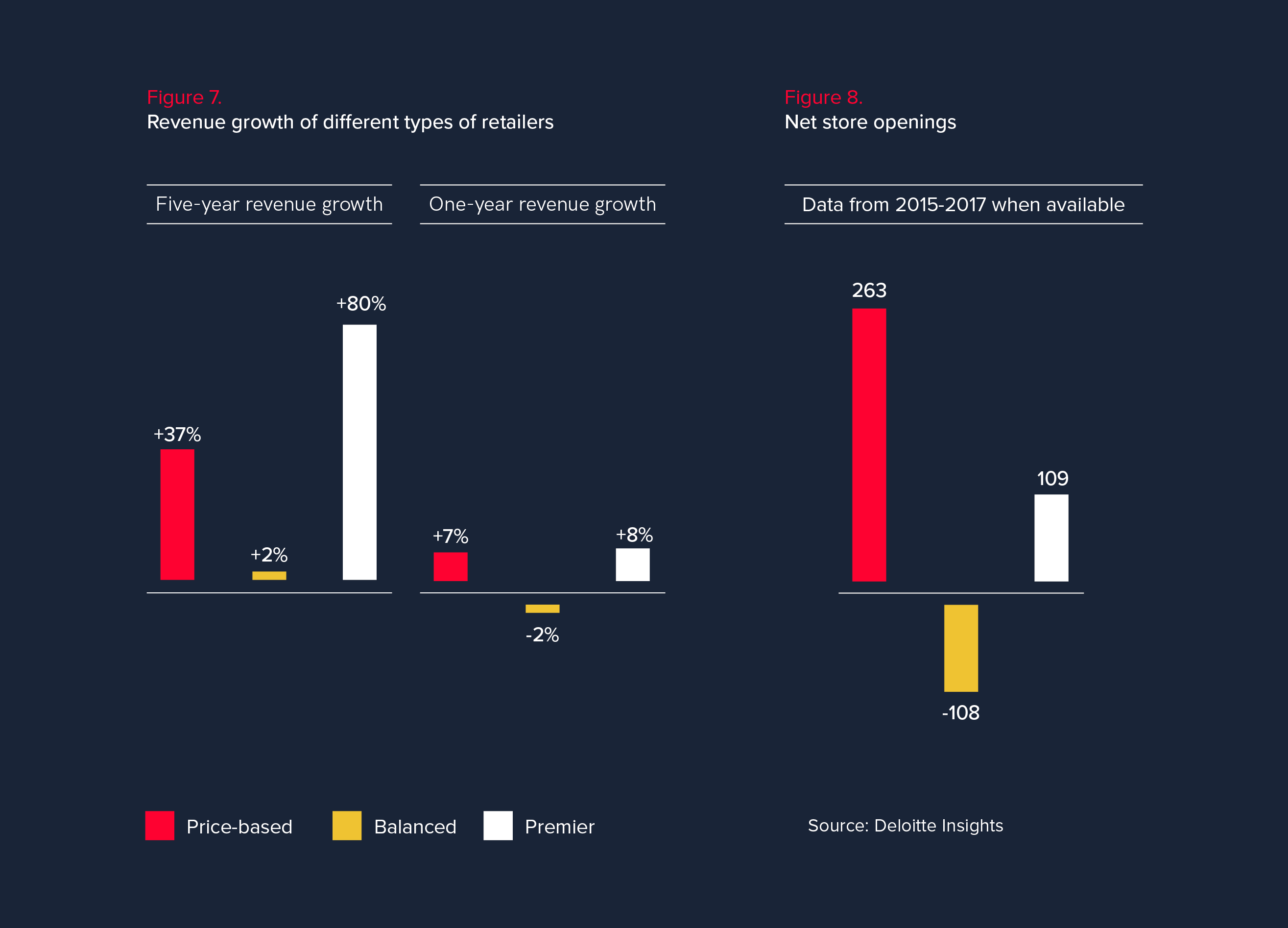

If we check under the hood, part of the explanation resides in the massive disparities between consumers. In the United States, the 1% received 82% of the wealth generated in 2017. Over the last decade, 80% of consumers have watched their economic situations deteriorate, causing irrevocable changes to their consumer habits. Shopping habits are intrinsically linked to income brackets and retail has been shifting as a reaction to America’s economic situation. Deloitte’s analysis separates retailers into three categories to glean a more detailed understanding of this phenomenon.

First, discount stores that base their market value in low, attractive prices. Second, more “balanced” retailers that rely on promotions, product variety and shopper experience. Third, retailers that offer differentiated high value-added products. According to Deloitte, the rupture between weak and strong revenues can be found among retailers.

If we look at retail sales according to economic status, the richest are making their profile group skyrocket. On the other end of the spectrum, smaller income and middle-class households are rushing to discount stores to compensate for their loss of buying power, leaving our second category of retailers without a solid clientele reference point. If understanding the consumer is the key to gaining footing in this industry, the companies that forgot to are paying the price.

Furthermore, today’s constant access to technology is transforming the habits and needs of consumers. Comparing products and prices is easier than ever before, and flow of access has opened the door to new competitors on the market.

46.6%

In the United States, the 20% richest segment

of the population held more than 46.6% of total incomes..

Source: World Bank

In a market where offering a personalized shopping experience fosters customer loyalty, retailers cannot forgo understanding their clientele. Retail is exploding into smaller, niche markets where each type of client brings their own set of unique expectations.

As a result, upscale malls are doing very well, such as Forum Shops at Caesars in Las Vegas, where sales per square feet stand at $1,400, and Yorkdale Shopping Centre in Toronto holding $1.653 per sqare feet in revenue. On the other hand, neighbourhood malls in Canada are struggling, while hundreds have closed in the United States since 2008.

Amidst all the upheaval in consumer demand, some shopping malls in Canada are adapting to the changes surrounding them by becoming specialized.

A select few, like the Yorkdale Shopping Centre, are reaping major benefits. What exactly is happening to the profit margins of shopping malls in Canada? Several factors play a part, including the rise of ecommerce, evolving consumer tastes, and the Millennial generation, who bring their own unique spending habits.

As per the Huffington Post, the rise of specialty retailers — like stand-alone stores for brands such as Hunter Boot Ltd and Canada Goose — and discount stores, including Walmart and Dollarama, are also luring shoppers away from former Canadian mall stalwarts like Sears.

Meanwhile, technological advances like smartphone cameras have eliminated legacy photography stores like Blacks. Online trading platforms like Bunz and Kijiji have lessened the need to buy new items.

Though demand has changed, Canada still dedicates an enormous amount of real estate to shopping centres: 16.4 square feet per person, compared with 2.4 in Germany, according to report from Cowen and Co.

Finally, the Millennials on which malls so desperately depend aren’t driving cars as much as their parents did, which reduces their mobility. They also prefer to spend money on experiences, like travelling, rather than on material things.

The result is that the savviest mall operators have been forced to change strategies and reinvent their spaces.

Yorkdale Shopping Centre has been a model example in that regard. According to the Globe and Mail, the North York mall lists annual sales figures of $1.6-billion, generated by 18 million visitors.

According to Jay Drexler, the national vice-president of retail leasing at Oxford Properties, which is the managing partner at Yorkdale, the centre began emphasizing a higher-end strategy about 12 years ago, beginning with the success of the shopping centre’s Holt Renfrew store. In 2009, Yorkdale’s first international luxury addition was Tiffany & Co. In the following years, the shopping centre added one new luxury brand per year, which recently increased to three or four annual additions, according to the Globe and Mail,

As Toronto’s upper class population grows, along with it comes a larger demand for high-end fashion, beauty, tech, and housewares. The Globe and Mail noted that all those international luxury brands with locations in the city’s Bloor-Yorkville neighbourhood are now targeting none other than Yorkdale for their second locations.

Yorkdale doesn’t just use luxury brands to entice new generations of shoppers. As Huffington Post explains, Yorkdale doubled down on food offerings that draw in shoppers and keep them inside longer, bringing in a Jamie Oliver restaurant and, more recently, Canada’s first Cheesecake Factory.

It’s all paying dividends, too: Yorkdale leads Canada’s malls in sales per square footage, according to the Retail Council of Canada.

Drexler sees the major shifts in consumer demand and bets there will be a bigger mix of retailers in the shopping centre, aiming to include a smaller concentration of fashion boutiques and more offerings in the beauty, home, tech and entertainment categories. Moreover, it could include popular e-commerce businesses that have chosen to open brick and mortar locations.

Clearly, this can’t be replicated across Canada. A mall in Moose Jaw, Saskatchewan simply isn’t blessed with the same foot traffic that Yorkdale attracts every day.

Armin Begic, director of the retail business group and market research firm NPD Group, told Huffington Post that malls in smaller cities will replace large anchors with multiple, smaller tenants featuring the type of experiences their customers want. An example of this type of creative retailer could be Indigo Books & Music Inc., with its cafes, book clubs and children’s toy areas.

Some have other solutions for malls in smaller centres, like turning them into mixed-use spaces with restaurants, dentist offices, gyms, and even condos.

The only certainty is that the times are changing, and these shopping centres are doing anything in their power to remain relevant. What’s also clear is that, in a shifting consumer landscape, places like Yorkdale Shopping Centre are reaping the rewards like never before.

A unique retail concept that involves creating a mini-mall within a larger shopping centre is preparing to expand to other venues following its successful debut at the West Edmonton Mall.

The Retail as a Service (RAAS) concept was launched at West Edmonton Mall last fall, allocating just over 5,000 square feet to a minimum of 20 local retailers, with the capacity to hold as many as 30.

Mark Ghermezian is the founder and CEO of RAAS, and part of the family that developed the West Edmonton Mall as well as other big international shopping centres. Ghermezian said the concept was introduced to help emerging and local brands that began their businesses online.

“We wanted to bring that sense of community and relevance of a brick and mortar experience to our environment and bring them all together under one roof,” said Ghermezian. It’s a place where those stores can open physical locations while also being supported by the community the mall is creating, he goes on to explain.

Another similar RAAS concept opened in November in another Ghermezian family-owned shopping centre: in Mall of America, in Minneapolis.

600 M

The total surface of shopping centres

in Canada is 600 million sq ft

Source: Ryerson University’s Center

for the Study of Commercial Activity

Michael Kehoe, an Alberta-based retail specialist with Fairfield Commercial Real Estate in Calgary, said the RAAS project is a great incubator for startup retail entrepreneurs and established retail brands that wish to set up pop-ups to test drive specific merchandise lines in a new market.

“The concept is transferable to other shopping centres or non-retail venues. RAAS is a throwback to the great Souks of the Middle East that were the world’s first shopping centres, some dating back over 1,500 years,” said Kehoe.

74,000

In total, Canadian shopping malls are housing over

74 000 retail stores and services

Source: Ryerson University’s Center

for the Study of Commercial Activity

“Many retailers that get their start in locations such as the RAAS — where store sizes are small, rents are often affordable and lease terms likely flexible — go on to lease brick and mortar stores and become long-term shopping centre tenants,” said Kehoe.

Kehoe is a commercial real estate professional with over 40 years of experience. He has worked for many years as a mall manager, marketing director and retail leasing executive. He is an ambassador for the New York-based International Council of Shopping Centers, where he has been a member since 1982.

Besides the West Edmonton Mall and the Mall of America, the Ghermezian family also owns American Dream in New Jersey and American Dream in Miami.

Innovative ideas are popping up everywhere to optimize the retail space malls previously filled with fast food chains and department stores.

Today, when a mall manager tries to make the most out of their expensive retail space, they think outside the box: they turn to micro-stores, residential units, entertainment venues and ephemeral stores.

As a result, gigantic venues are no longer attractive, while highly flexible and specialized tenants are filling up vacancies. In other words, small is beautiful.

More square footage no longer means more sales, as many big box retailers have shut down and many shoppers prefer the convenience of online shopping. Meanwhile, commercial rents have increased both in the US and Canada, especially within desirable postal codes. As a result, retailers are increasingly maximizing their square footage and implementing “smaller is better” strategies, while mall operators are building out spaces to accommodate them.

“Downsizing” and “rightsizing” are two terms with similar meanings, yet they often translate very differently within the context of the retail sector.

Downsizing mostly refers to planned shutdowns of retail locations and laying off a substantial number of employees. The primary motive is to reduce labour and operating costs and therefore comes with a negative connotation.

On the other hand, rightsizing is a more positive concept. Rightsizing occurs when a company restructures its human resources to align with company goals and strategies. This may include a combination of department and position cuts to make room for a more efficient use of a store’s existing square footage, based on customer demand and preferences.

US-based department store chain Kohl’s recently adopted a rightsizing strategy with encouraging results. Kohl’s has shrunk hundreds of stores in its fleet of 1,160 locations from 90,000 square feet to about 60,000. Furthermore, the company is developing an even smaller 35,000 square foot store model at 12 locations hoping to reach new markets, including downtown locations.

This rightsizing strategy aims to maintain brand presence, improve inventory management through “unsexy but essential technologies” and help support e-commerce activities, given that many shoppers prefer to pick up orders in-store (online shopping represents 18% of the company sales as of April 2018). During the holiday quarter, Kohl’s sales rose 6.3%, aided by a 7% drop in inventory.

There are retailers that are taking the rightsizing approach much further with “micro-stores.” In September 2017, Nordstrom, the US-based high-end clothing department store chain, announced the launch of Nordstrom Local. Nordstrom Local has a minimal 3,000 square foot footprint, significantly smaller than the average 140,000 square foot Nordstrom store.

$1,257

The average sales per square feet in the 10 most

productive Canadian shopping centres is $1,257

Source: Retail Council of Canada

This concept store has no dedicated inventory: customers have access to personal stylists (who can transfer merchandise in for customers from other locations) as well as a suite for convenient services such as in-store pick up for online purchases, an alterations and tailoring service, and manicure appointments. Customers can also make returns at Nordstrom Local from Nordstrom stores, Nordstrom.com and Trunk Club.

A variant of the micro-store is the “ephemeral store,” commonly referred to as “pop-up shops.” They are basically tiny stores that temporarily reside in a vacant standalone commercial venue or within an occupied structure.

“Designed to share a unique experience and experience pleasure of discovery, they have little time to seduce, but are likely to mark the imagination for a long time… Entering an ephemeral shop means discovering new urban territory. Located in atypical venues, these stores often offer an amazing decor and allow a meticulous staging of products. Customers appreciate seeing the brand they love showcased in an unusual environment,” explains events agency Make it Happen in a recent blog post.

Montreal-based Aldo Group, a global chain of shoe and accessories stores, began employing this strategy as early as 2011 with its “Call It Spring” brand, placing pop-up shops inside 600 JCPenney department stores across the US.

Facing a potentially “doom and gloom” landscape, retailers are becoming more and more creative and efficient with their square footage utilization. The future of retail is bound to become smaller, niftier and more personalized.

Large spaces formerly occupied by anchor tenants continue to sit unclaimed in Canadian shopping centres. However, there is hope amidst this stressful time for retail landlords.

Colliers International, a commercial real estate firm, recently came out with its national spring retail report. It stated that 20 percent of vacated Target stores have yet to be filled. The rest have been leased to other retailers.

Target Canada was the Canadian subsidiary of the Target Corporation, the second-largest discount retailer in the United States. The retail chain may have had 133 Canadian locations in March 2013, but they slowly racked up $2.1 billion in losses, ultimately filing for bankruptcy and shutting all its stores by April 2015.

In a competitive marketplace, a mall’s anchor could determine whether the rest of the tenants are profitable or not.

Sears is another example of a fallen giant on Canadian soil. Once a Canadian retail staple, Sears gradually closed all its stores by the end of 2017. In its report, Colliers said landlords have to be creative in filling the void anchor tenants like Target and Sears have left in their wake.

“The importance of a mall anchor depends on what else is available at competitive malls and shopping areas. In a competitive marketplace, a mall’s anchor could determine whether the rest of the tenants are profitable or not,” said James Smerdon, Director, Retail Consulting for Colliers International.

According to Colliers, it’s not all doom and gloom for Canadian shopping centres. In fact, the disappearance of prime Sears locations across Canada has been (or will be) replaced with several retail chains such as Nordstrom, La Maison Simons and Saks Fifth Avenue.

Meanwhile, retail sales are still growing. The Colliers report said total national retail sales in 2017 amounted to $588.83 billion, a 6.46% increase from 2016.

American Malls Are Dying Like FliesShopping malls are falling like flies in the United States. Two hundred american malls disappeared in 2016 alone. According to REIS, the average vacancy rate in the United States was 9.1% at the beginning of the year, with rents similar to those of 2006! Of the 1500 current US shopping centers, 10% will disappear within the next two years, say the CoStar Group real estate analysts, as quoted by the New York Times. There is even a website dedicated to the subject: www.deadmalls.com. |

Reviving a shopping mall that is losing momentum is difficult and risky business. When you lose giants like Sears or JCPenny and grass is growing between the cracks in the parking lot, it doesn’t look good. On the other hand, huge parcels of land, strategically located near major roadways, provide undeniable advantages.

In fact, some struggling shopping centres are converted into warehouses for Amazon, university campuses, office buildings, hospital centres, or churches. “I predict that three quarters of them will be converted according to lifestyle,” said Ben Conwell, a retail expert at Cushman & Wakefield, an American commercial real estate broker.

In fact, reviving a dead mall is more like avant-garde urbanism.

“You don’t drive there, you live there!” was a headline in the Globe and Mail this past May, reporting on the redevelopment of the Honeydale Mall in Toronto. Soon, there will be several condo towers, green spaces and new businesses along the streets.

«Cities are gradually moving from an automobile-dominated culture to mobility-based on a mix of means of transportation,» said Brent Toderian, President of the Canadian Institute of Planners.

Shopping centres surrounded by a sea of asphalt will be converted into urban green spaces, where public transport, walking, cycling and self-driving shuttles have replaced automobiles, which have been relegated, at worst, to underground parking lots.

Cities are gradually moving from an automobile-dominated culture to mobility-based on a mix of means of transportation.

Even better, hotels and theatres are joining the ranks in shopping centres, as demonstrated (successfully) at the DIX30, in Brossard, which will soon become the Montreal South Shore terminal for the Réseau express métropolitain managed by the Caisse de dépôt et placement du Québec.

In Englewood, Colorado, a new downtown area was created on the former grounds of the Cinderella City Mall, once the largest shopping centre west of the Mississippi. A light rail train now provides public access to a civic centre, apartment buildings and a smaller version of the old-fashioned shopping centre, which is busier than ever.

In Vancouver, 14 new 44-storey towers are being constructed in the skyline of the Oakridge Centre, featuring green roofs, 2,600 apartments, 500,000 square feet of office space, one million square feet of pedestrian street shopping, and 10 acres of green space. Sales now total $1,600 per square foot, the second highest in the country, according to its promoters.

In Virginia, Crosland Southeast has partnered with Richmond County authorities to convert a decaying mall into a new urban neighbourhood with a Kroger supermarket, multiple apartment buildings with more than 1,000 apartments, a Walmart Supercenter, and a green space. Without the cooperation of elected officials, the project, which surpasses $120 million USD, would not have seen the light of day, said H. Garrett Hart III, Director at Chesterfield Economic Development.

«Not all consumers want to buy online. The tactile experience of shopping, the crowd, and the excitement remain in the collective psyche,» wrote Eric Rothman, manager at CenterSquare, in the Commercial Property Executive.

What’s on the menu? Upscale restaurants, climbing centres, and indoor theme parks, in addition to open spaces for shows, tournaments, theatrical performances, circus activities, free yoga classes, family movies and giant interactive screens, like the three-storey Samsung 837 multimedia wall located in New York’s Meatpacking District.

0.1%

Between 2012 and 2017, department store revenue

fell by an annualized rate of 0.1% to $28.1 billion.

Source: IBISWorld

Amazon’s vision “to be earth’s most customer-centric company” had a huge impact on the retail industry as a whole. It single-handedly made customer centricity a top priority for many retailers.

Today, the best performers understand that acquiring new customers is five times more expensive than keeping existing ones. As a result, shopping centres are trying harder than ever to understand their clients and delight them in every possible way. The industry has taken many different paths to reach this goal.

Mall owners that outperform the competition understand that because they are in the retail business, they have to measure everything they can about their shoppers. Measuring foot traffic and sales per square foot isn’t enough anymore. Today, as consumers no longer have to come to malls, malls are striving to know as much about their shoppers as Amazon knows about theirs.

Just like retailers, malls are investing in rewards programs and indoor navigation apps and other systems to gather data about their shoppers, from traffic flow to customer feedback. Those investments are paying off. According to a Deloitte Digital survey (Consumer Experience In The Retail Renaissance), retailers that are investing the most in data aggregation and analysis have seen a revenue increase of more than 10% in the past fiscal year.

Westfield was one of the first large mall operator to invest massively in big data. In 2012, it set up Westfield Labs, an innovation lab that developed a comprehensive solution to track client traffic flow and purchases across all the retailers in its malls, and share the collected data with them.

Following the sale of Westfield to Unibail-Rodamco in 2017, Westfield Labs was spun-off into an independent company called OneMarket. Following suit, OneMarket commercializes its integrated solutions to malls and retailers as well.

Pooling the data collected by mall operators and retailers alike allows shopping centres to deliver a better experience to shoppers across their entire journey. It helps them make better decisions in terms of to whom they rent out their retail space, what stores should be where, and so on. Furthermore, such a system allows malls to improve the customer experience of their shoppers, by offering useful services, such as digital receipts, across all their retailers.

$1.25 trillion

The global chatbot market is expected to reach

USD 1.25 billion by 2025 with an annual growth rate of 25%.

Source: Grand View Research, Inc

TALK TO A ROBOTDigital conversational agents, commonly referred to as “chatbots,” are becoming more and more common in malls. These chatbots allow malls to leverage data to provide a better customer experience and collect customer feedback. The Mall of America in Minnesota (the biggest shopping centre in the United States) has recently launched a conversational agent initiative. In December 2017, the mall introduced a new app designed by Satisfi Labs. It is available via the Mall of America website, mobile app, Facebook page, and Amazon Alexa. Additionally, three semi-humanoid Pepper robots conceived by SoftBank Robotics are on hand to guide lost shoppers to their desired store or attraction; and can even provide suggestions. |

While mall operators need data to understand the traffic flow of shoppers within their space, shoppers often struggle to find specific retailers once inside a mall. Needless to say, that is a business opportunity in itself. According to a report from MarketsandMarkets, the indoor location market could be worth $41 billion by 2022.

Such systems use a number of technologies such as WiFi, radio waves and magnetic fields. Many current systems utilize WiFi or Bluetooth beacons installed around a given location, which can communicate through a user’s phone and offer real-time directions similar to GPS.

Toronto-based Mapsted eliminates the need for beacons, potentially making it more cost-effective than other indoor navigation offerings. It works without WiFi, Bluetooth or an internet connection. Users simply launch the Mapsted app and start navigating. Mapsted requires no data connection and uses very little battery power, therefore it can be efficient and cost-effective for users as well.

On average, an industry’s Net Promoter leader outgrows its competitors by a factor greater than two times. It’s not surprising that the Net Promoter Score (NPS), a measurement of client satisfaction, has become a reference point for shopping centres.

Shopping malls are using various strategies to perform NPS surveys. Many of them employ their mailing list to survey their clients, using anything from their WiFi network to an indoor navigation app to retrieve their shoppers’ email addresses. Other ways to perform NPS surveys is to have surveyors question shoppers as they exit the mall (intercepts), or to perform social media surveys with providers such as POTLOC.

NPS can be an excellent Swiss Army knife for the industry, capable of obtaining different information according to the surveyed population. Here are three audiences malls are targeting: shoppers that visited a mall over the course of the last 12 months, shoppers that are shopping at a competing mall, and specific population segments that are part of the mall’s client base.

According to Bain & Company, NPS is an excellent indicator of potential growth. We’ve seen it happen: the business with the best NPS in their respective industry grows twice as quickly as their closest competitors. Based on this argument alone, brands have become increasingly interested in NPS. Furthermore, if your shopping centre receives a high score, it can add value to your recruitment process when searching for quality tenants.

Many brands, such as Loblaw or Jardiland, base a part of certain employees’ salaries on NPS, rendering them dependent on client recognition.

Discover crowdsourcing; how placing consumers at the heart of the experience allows for an understanding of their shopping habits and needs with POTLOC

Potloc reinvents retail market research.

REMERCIEMENTS:

Rédacteurs: Jérémie Caussin, Stéphane Desjardins, Mario Toneguzzi, Phil Siarri, Joseph Czikk, Philippa Brangam.

Directeur Marketing: Antoine Théorêt-Poupart.

Directeur de contenu: Julien Brault.

Designer: Xavier Labaye